Quantum computing just got its first traditional IPO.

Technology Watch – Quantinuum |

|

Quantinuum listed this month with high conviction fundamental investors like Janus Henderson, Fidelity, and the US Government joining Honeywell, Nvidia, Mitsui, Amgen et al on the cap table. Being in New York for the float, we could clearly observe that this is a long term strategy for Honeywell. They acted as the primary anchor for the listing and only diluted down slightly their dominant voting control. It is also early days. We need to wait for the release of the next generation hardware with 100 logical qubits in 2027 (fingers crossed, and hopefully a cloud-based release early in the calendar year). Quantum Computing remains one of the most fascinating long-term technology themes. It is our conviction that the combination of continuing breakthrough science alongside and patient institutional and corporate capital will place Quantum Computing firmly on the strategic compute layer. The real unlock will occur with fault tolerance, error correction, and hybrid quantum/classical workflows, replicating how AI utilises GPUs today. The reason to pay attention to Quantinuum is their logical qubit count. The stopwatch does not lie. Most quantum architectures require thousands of physical qubits to produce a single error-corrected logical one. Quantinuum does it at two-to-one. Rather than fixed qubits talking to their immediate neighbours, Quantinuum’s trapped ions physically move around the chip, so any qubit can interact directly with any other. There’s no fidelity loss from this type of daisy-chaining. The 2027 architecture will extend this into a 2D junction lattice, where scale becomes a matter of adding tiles rather than reinventing the physics. |

Market Watch – SpaceX |

|

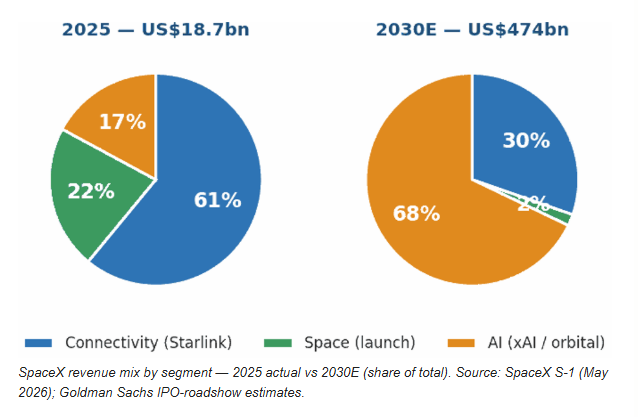

Without commenting on the capital transaction, and just looking at what is under the hood, SpaceX is three businesses bolted into one platform. US$18.7 billion FY25 revenue split across three segments: Connectivity (Starlink) at US$11.4 billion, or 61% of the total; Space – launch services, Falcon and Dragon, and government missions – at US$4.1 billion, or 22%; and a newly consolidated AI segment, xAI, folded in via the February 2026 all-stock merger, at US$3.2 billion, or 17%. The bull case is that the three segments feed one another. Cheap, reusable launch drops the cost per kilogram to orbit; this, in turn, lets Starlink deploy a constellation no rival can afford to match; Starlink’s high-margin subscription cash then funds Starship and the next wave of capital spending; and Starship, in turn, becomes the vehicle that lifts the next business, compute, into orbit. The bear case of the equity story is essentially that the orange piece of the pie in 2030 with all the unknowns and competitive environment is too much. SpaceX is striving to deploy orbital AI-compute satellites by 2028 – solar-powered data centres in orbit that avoid the power and land supply issues currently restraining terrestrial AI. The long-run ambition stretches belief: a constellation of up to one million satellites, each roughly a tonne and carrying about 100 kW of compute – on the order of 80-150 GW of capacity drawing on effectively free solar energy, with Starlink supplying the low-latency downlink. Launch cadence is the metric that will truth out this whole story – every satellite, every orbital data centre and every dollar of launch revenue has to physically get to orbit. In 2025 SpaceX flew roughly 170 missions, its sixth consecutive annual record, lifting some 2,213 tonnes or 80% of all mass launched worldwide. Musk’s stated ambition by 2030 is exponential (and probably unachievable): one launch per hour, or roughly 8,000 a year. The US East and West Coasts (Vandenberg, Cape Canaveral, Starbase) face a compounding set of physical and regulatory constraints: airspace congestion, weather windows, range safety queues, population proximity, and regulatory timelines. When there are 160+ SpaceX missions a year, plus Blue Origin, Rocket Lab, ULA, and a dozen smaller providers all competing for the same windows, the geography of launch becomes a strategic asset. The pace of launch is no longer constrained by rocket technology or manufacturing. It is increasingly constrained by where and when you are permitted to launch – and who controls that real estate. Australia’s geography offers something no amount of rocket engineering can solve: wide open airspace, sparse sea traffic, stable year-round weather, and no adversarial regulatory overlap with US authorities. Southern Launch’s multi-use model (re-entry, hypersonic testing, orbital launch etc) overcomes all these constraints. Varda Space Industries has already contracted 20 further spacecraft returns to Koonibba following the historic W-2 landing in February 2025 (discussed in our May Newsletter). |

Sovereign Watch – Protecting Private Capital Formation in Australia’s National Priority Areas

|

|

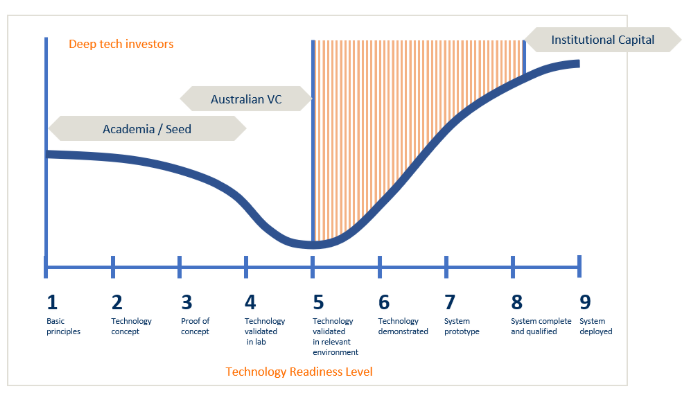

Australia’s proposed Capital Gains Tax changes arrive at a pivotal moment for the nation’s sovereign industrial ambitions. While the broader policy community supports welcome reforms to ESIC and ESVCLP provisions that help early-stage start-ups, we argue that a critical and largely unaddressed funding gap will remain. At Technology Readiness Levels 5–8, where laboratory-validated technologies must be scaled into new manufacturing jobs and sovereign capability, private capital is already thin. The proposed CGT changes risk making that gap structural and permanent. The National Reconstruction Fund was designed to anchor sovereign investment and catalyse private co-capital in exactly these TRL 5–8 companies. If new CGT rules disincentivise the private investors who sit alongside the NRF, the Fund cannot fulfil its mandate and Australia’s National Priority Areas in space, quantum, cyber, critical minerals and advanced manufacturing will lose the private capital they urgently need to reach production scale. Powerhouse Venture Partners has made these points in our submission to Treasury. |

|

Disclaimer: This blogpot is for informational purposes only, it does not constitute investment or financial advice. Nothing here constitutes an investment offering of any kind, unless expressly stated. Before acting on any information contained in this blogpost, each person should obtain independent taxation, financial and legal advice relating to this information and consider it carefully before making any decision or recommendation. The Powerhouse Group of Companies holds an Australian financial services licence (AFSL# 497505) and may have a shareholding in some companies discussed. Visit our website to read our privacy policy. |